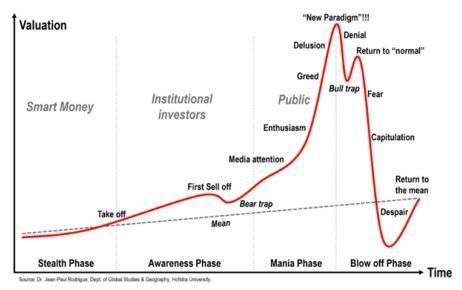

A Bubbly World

There are two constants investors should remember when investing in potential bubbles – markets always go too far, both up and down. And gravity exerts its force, inevitably.

Markets change over time and we would contend many of the changes in the past decade have contributed to a market more susceptible to forming bubbles. Not the same as some of those past ‘mega bubbles’ that can rock the entire market, smaller ones that don’t seem to last as long but still share similar characteristics. Below are some of the contributing ingredients or seeds that are contributing to a more fertile market for growing bubbles:

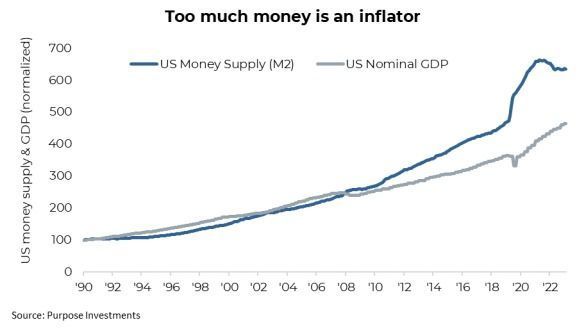

Too much money - The money supply has historically grown somewhat in line with nominal GDP. But in the 2010s, it started to grow much faster – a follow-up response to the financial crisis. This resulted in a rising savings rate as well. Both these trends exploded to the upside in 2020/2021 due to the pandemic. It was a period in which many mini bubbles inflated – crypto, disruptive tech, and even used video game retailers. The list was long.

In 2022, many of those mini bubbles deflated as money growth began to contract, central banks raising rates, etc. And also, many of those mini bubbles went too far. The gap between the economy and money supply is improving, which may be a risk to anything in bubble territory today. Yet there is still way too much money floating about, which is one of the fuels for a bubble.

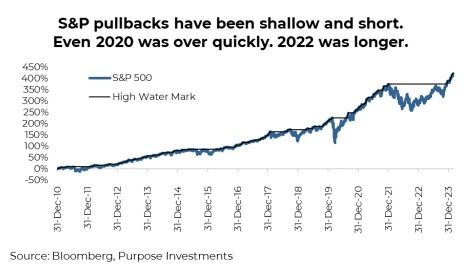

Fearless investors – For investors who have only experienced markets after the 2008 financial crisis or for those with short memories, it has been a rather pleasant experience. From 2010 till 2020, declines in the equity market tended to be shallower and shorter in duration than in previous decades. Markets would drop and recover pretty quickly, encouraging the ‘buy the dip’ mantra. Then, the pandemic drop in 2020 solidified this view, as the drop may have been bigger, but the bounce back was incredible.

2022 threw some cold water on this strategy of buying any weakness, yet with markets now making new highs, the buy-the-dip mindset appears alive and well. Investors just don’t seem to be fearful anymore, which is another key ingredient for bubbles.

Less Fundamentals – Everyone probably believes the value of something is its price in the market. Apple closed at $179, making it worth $2.8 billion based on its price. Maybe. The price of any asset in the market is where the marginal seller and marginal buyer meet. If there are more motivated buyers than sellers, the price rises until the higher price entices more sellers.

Yet more and more volume is driven by passive investment vehicles that are simply transacting due to flows and give no thought to the price. Add to this trade flow momentum strategies, HFT, option book managers, etc. None of which will say Apple is worth more or less than $179. They are price acceptors, accepting whatever the price is.

Countering this group is active managers or investors, that have a view on the value of an investment and will often transact if that price gets too far away from their perceived value. They do not believe value equals price and attempt to profit from the discrepancy. The problem is over the past decade, the amount of money in price-accepting strategies has kept growing faster, and the active group has kept shrinking.

We are not saying the market pricing mechanism is broken. However, this increasing tilt has created a more fertile market for bubble formation. Price and value can become very distant from one another.

Access – One steady trend is the democratization of investment strategies. If you wanted to buy one of the nifty 50 stocks in the 1970s, you probably had to call your broker to instruct them to buy some shares of Xerox or Avon. Today, with a tap on your smartphone, you can buy shares of Nvidia, trade some bitcoin or buy an ETF that holds companies focused on cyber security.

Easier access is a sign of progress. Making things better, faster, cheaper or easier is how our economy progresses. Easier access has also made investing more fun and exciting. It has also given rise to more speculators or investors throwing a bit of money at a more speculative investment idea. Call it play money or mad money; there is a lot of it out there.

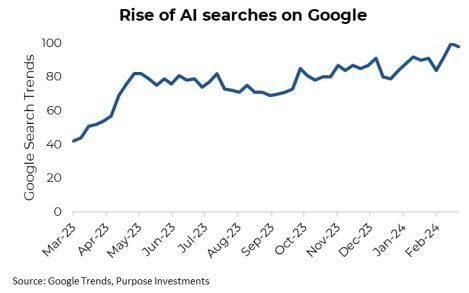

Social Media – Information travels faster than ever, which means ideas travel faster, too. The Reddit crowd lifted a near-bankrupt used video game retailer from a few hundred million market cap to over $20 billion. The company is back down to $4 billion and has been losing money since 2019. This is an extreme, but the speed at which ideas become mainstream has dramatically increased over the years.

The speed of ideas or thought dispersion across investors likely feeds quicker bubble formation than in years past. Just look at the Google search trends for Artificial Intelligence.

Before we dive into investment strategies for a bubblier world, let’s all just realize it is our behaviours that create these bubbles. Much about bubbles can be grounded in behaviour finance and momentum.

Biases & Bubbles

Market momentum refers to the tendency of asset prices to persist in their current trend. In essence, it's betting on the winners. While there isn’t a single individual credited with “proving” the momentum factor, it’s been widely documented by many academics across various markets for some time. This factor can be quite powerful, but it is also a double-edged sword. It contributes to the formation of bubbles, driving asset prices to levels that deviate significantly from their intrinsic values. There are many explanations behind market momentum as a factor. Some technical but most explanations rely heavily on the work of behavioural finance.

The behavioural biases behind momentum:

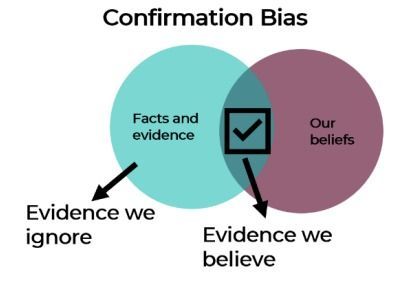

Anchoring and Underreaction: Tendency to overweight the importance of the first information that we learn. Social anchoring can also increase pressure toward conformity and acceptance of the status quo. It tends to anchor investor expectations to past performance, such as extrapolating past trends into the future. One way it can fuel momentum and contribute to bubbles is it causes investors to underreact to news initially, which keeps prices below fair value for too long. Once price trends do finally develop, they remain strong for some time as prices catch up to their ‘fair’ value, and often go beyond. Confirmation Bias: Closely related to anchoring is confirmation bias. It’s the tendency to overemphasize the importance of information that reinforces our view while ignoring contradictory evidence. The bias can reinforce momentum by focusing investor attention only on information that supports the current dominant narrative, ignoring warning signs at their peril. In general, we look at price moves as representative of the future we want to see and may invest more in securities that have recently done well and less in those that have not done as well, thereby causing stocks to trend for too long.

Herding: Herding is a strong physiological as well as psychological bias. It’s primordial; we’re physically wired to prefer the pack, and it is associated with the release of oxytocin, reinforcing the positive feelings of trust and security. It’s far more natural as an investor to jump on the bandwagon and ride the wave with the rest of the herd, even if we see it fast approaching the rocky shore. As humans, we think in herds, go mad in herds, but only recover our own senses slowly, and one by one.

Overconfidence – This bias is simply believing your skill and ability are greater than they really are. We’re all prone to overestimate how much we understand about the world and to underestimate the role of luck. The sad reality is that overconfidence can lead to suboptimal outcomes; it is the strongest swimmers who are more likely to drown. Overconfident investors underestimate the risks associated with momentum-driven markets, leading them to engage in excessive buying without fully considering the fundamentals, which contributes to bubble formation.

Not only that, but overconfidence also triggers other biases, such as hindsight bias as well as self-attribution bias. In a raging bull market, it is easy to attribute success to skill, causing investors to buy more, which only pushes prices higher.

Disposition Effect: Investor s tend to sell winners too early in order to lock in gains while holding onto losers too long in the hope they will make back what they lost. It also brings in ideas around prospect theory and mental accounting. How often have you heard that it is only a loss if it is realized? When negative news hits, investors can be reluctant to sell stocks that have had a strong run. This action delays the price discovery prices, which contributes to the momentum effect and continuation of bubbles until investors react all at once.

Besides the behavioural factors behind momentum, there are also a number of structural factors as well. These include liquidity constraints, transaction costs and a delay in adjustment to new information that leads to trends. Investors with different time horizons react to news and events at their own pace. The staggered approach can supply enough sustained buying and selling pressure to begin the feedback loops that the behavioural biases thrive on.

Reflexive Bubbles

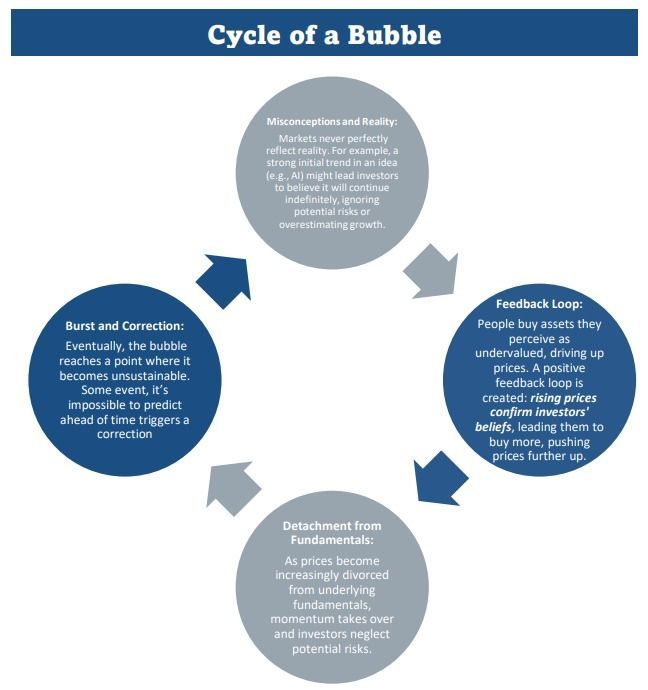

For anyone who has read Soros, this theory should sound familiar. Positive feedback between prices, expectations and economic fundamentals prevents economic equilibrium. At its core, the theory of reflexivity offers a unique perspective on how stock market bubbles can develop. In an efficient market, bubbles wouldn’t exist. The Theory of Reflexivity focuses on the interactions between market participants' perceptions and reality. Here's a simplistic graphic on how it applies:

Investing in a Bubblier World

If we are living in a world more prone to bubbles (or mini bubbles), should our investment process change? And how do you make money from bubbles while protecting yourself from a bubble’s downside? We believe there are a few components that are crucial for success: 1. Early bubble identification 2. Prudent exposure – sizing 3. Rules

Early bubble identification – This is more challenging than you would think. There is a lot of content about how the future of society might look, and some of this is really well-founded. No doubt AI has taken off; what about nuclear fusion or quantum computing? You never know when the market is going to start getting excited about the next one. Or, in other words, when will a theme or idea start going mainstream, which is a prerequisite of a bubble?

One option is to do a ton of reading and research about future trends and become a futurist of sorts. And then place small exposures on many ideas. Call it diversification across ideas. Another option is to use momentum. You won’t be in before the bubble starts to inflate, yet price appreciation may identify a bubble early enough to hop on board. There will be false starts with using momentum, but much less reading is required.

Prudent exposure – sizing – If it goes up 50% in a year, it can just as easily go down 50% in a year. This is higher risk investing, which requires risk controls. One effective approach is sizing relative to an overall portfolio. Essentially, not risking too much. And while invested, revisiting the size or rebalancing can address portfolio drift risk.

In the very early days, sizing could be smaller. As a bubble continues to go mainstream, increasing and as the position becomes a size risk in a portfolio, begin harvesting.

Rules - The difference between a strong bull market and a bubble is not always clear at the moment. Only in hindsight does the bubble stand out. Feelings of regret are plenty. Regret of selling too early, or not selling all. In this aim, investors ideally ride the bubble all the way to the momentum battleground. It’s the area where market momentum encounters resistance either from investors employing contrarian strategies or simply from the gravity imposed by the dislocation of underlying economic realities and valuations. The battleground is where the tug of war begins and where astute investors can read the signs and see the tide of sobering rationality ahead.

There is no simple rule to put in place rather rules-based strategies using the power of trends, market technical and our behavioural biases can all add sell discipline and help provide an exit strategy. By taking profits when momentum begins to stall or sentiment begins to swing. Investors with a nuanced understanding of momentum, market psychology, risk appetite and the fundamentals can increase their chances of adeptly manoeuvring around the battleground. Some of the more useful strategies include:

Trailing stop-loss orders – Simple trailing stop-loss orders or selling targets based on deviation from recent highs can help lock in profits and limit losses as momentum wanes. Moving the stop-loss orders as prices move higher helps to mitigate the risk of holding onto a stock for too long during a bubble.

Contrarian Signals: Investors can incorporate contrarian indicators or sentiment measures to find potential turning points in market trends. By monitoring sentiment indicators for signs of excessive optimism or pessimism, investors can add sell discipline by exiting positions when sentiment reaches extreme levels, potentially signalling the peak of a bubble.

Technical indicators: These can be a useful way to measure trend strength and identify breakdowns, such as moving averages, volatility bands or relative strength.

Rebalance Discipline:

The KISS principle stands for "Keep It Simple, Stupid." It is a widely recognized principle that suggests simplicity and clarity should be always prioritized. Managing risk in an investment bubble doesn’t have to be complex. One of the simplest ways investors can manage risk is simply to rebalance. Portfolio rebalancing isn’t sexy, it doesn’t attempt to time the market, but rebalancing based on predetermined criteria whether time based, or value-based, trims overvalued positions and reallocates capital to undervalued assets. It adds discipline to the investment process, and discipline is a key ingredient to building long term wealth and not chasing short term gains.

Market efficiency would argue against the existence of momentum and even bubbles. Markets can be mostly efficient, but the argument that the price is always right is absurd. When you think about efficient markets, Markowitz probably comes top of mind, but I think about Bob Barker and Adam Sandler. Bob Barker always argues the ‘Price is Right’, while Adam Sandler aka Happy Gilmour famously noted “the price is wrong $!&@#”.

The Final Word

Bubbles are fun, exciting and dangerous. They also appear to be increasingly widespread. Having a thoughtful, disciplined approach that incorporates some hard trading rules can go a long way in enjoying success in our bubbly world. It does offer the potential for strong returns. We prefer using momentum as both a buy and sell signal. True, we blame bubble creation in part on momentum trading; the key is to avoid being late. Too late to hop on board and too late to exit are the biggest risks. Momentum can provide a defence against this risk.

Source: Charts are sourced to Bloomberg L.P. and Purpose Investments Inc.

The contents of this publication were researched, written and produced by Purpose Investments Inc. and are used by Echelon Wealth Partners Inc. for information purposes only.

This report is authored by Craig Basinger, Greg Taylor and Derek Benedet Purpose Investments Inc.

Disclaimers

Echelon Wealth Partners Inc.

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Echelon Wealth Partners Inc. or its affiliates. Assumptions, opinions and estimates constitute the author's judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. The comments contained herein are general in nature and are not intended to be, nor should be construed to be, legal or tax advice to any particular individual. Accordingly, individuals should consult their own legal or tax advisors for advice with respect to the tax consequences to them.

Purpose Investments Inc.

Purpose Investments Inc. is a registered securities entity. Commissions, trailing commissions, management fees and expenses all may be associated with investment funds. Please read the prospectus before investing. If the securities are purchased or sold on a stock exchange, you may pay more or receive less than the current net asset value. Investment funds are not guaranteed, their values change frequently and past performance may not be repeated.

Forward Looking Statements

Forward-looking statements are based on current expectations, estimates, forecasts and projections based on beliefs and assumptions made by author. These statements involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. Neither Purpose Investments nor Echelon Partners warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. These estimates and expectations involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Unless required by applicable law, it is not undertaken, and specifically disclaimed, that there is any intention or obligation to update or revise the forward-looking statements, whether as a result of new information, future events or otherwise. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional

advice.

The particulars contained herein were obtained from sources which we believe are reliable, but are not guaranteed by us and may be incomplete. This is not an official publication or research report of either Echelon Partners or Purpose Investments, and this is not to be used as a solicitation in any jurisdiction.

This document is not for public distribution, is for informational purposes only, and is not being delivered to you in the context of an offering of any securities, nor is it a recommendation or solicitation to buy, hold or sell any security.

Share this post