The Calm Before the Calm

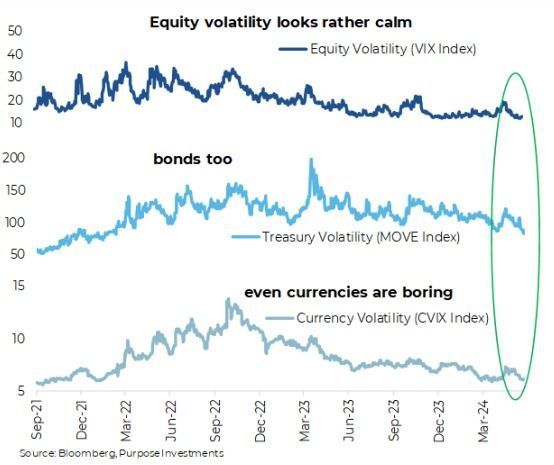

The volatility in the bond market has gone super low (2nd panel in chart). The MOVE index measures volatility in U.S. Treasury Bonds [actually at-the-money options on interest rate swaps, but let’s not go down that rabbit hole]. Even though bond yields moved higher this year, the 10-year started at 4%, gradually up to 4.75%, then back down to 4.5%; these moves pale in comparison to the last couple of years. In case you forgot, the same bond in 2022 went from 1.5% to 4.0% and in 2023, yields oscillated between 3.5 to 5.0%. Looking beyond Treasuries, credit spreads are back down to or close to historical lows. Investment Grade spreads in the U.S. are 50bps. Lows in past mini-credit cycles have been 40-60bps.

Yawn.

Or consider this: the S&P 500 has not had a 2% down day in 316 trading sessions dating back to February 2023. Third longest streak this millennium. Given this, it is not too surprising the VIX, which measures the implied volatility of S&P index options, is sitting down at 12 ½. The VIX uses near-term options for its measurement of volatility; even more surprisingly, the six-month VIX is dormant. Over the next six months, we will have endured a U.S. election (if it ends as scheduled) and perhaps a pivot from the Fed on interest rates. Even 5-6% out-of-the-money puts for December are only pricing in 16% volatility.

Insurance is cheap.

There is likely some downward pressure on option volatilities due to the proliferation of option strategies, especially those that write options. But given volatility has become so calm across so many markets and asset classes, we can’t really blame those yield-hungry investors.

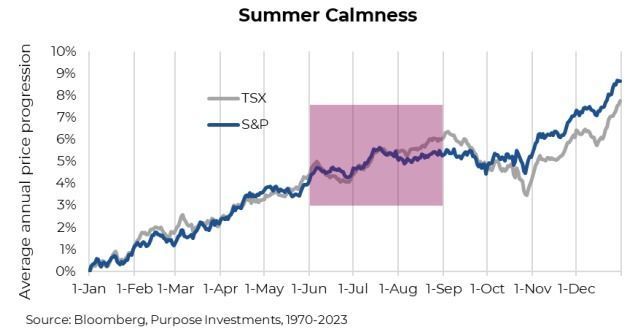

The question becomes, will this calmness persist? Maybe. There is no denying that, on average, markets tend to be relatively calm during the summer months (June through the end of August). All the traders/investors off in the Hamptons, Muskoka or wherever the Londoners go could make volumes lower and have fewer folks making big changes to their portfolios. Of course, averages can be very misleading and much variation can occur. With data back to 1970, the summer months are roughly flat on average for the S&P and the TSX. A seasonal chart for the VIX also shows this calmness as volatility falls in the summer months before moving materially higher in the often challenging September/October period.

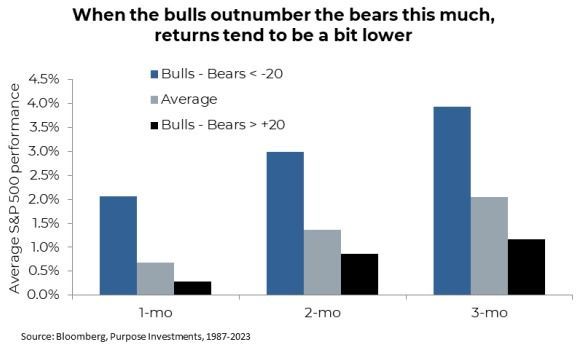

Not surprising that markets are gently trending higher with limited volatility; investors have become rather calm as well. In the latest survey, 47% of folks are bullish (AAII survey). Meanwhile, 26% are bearish, and 27% are neutral or undecided. We would highlight that from a sentiment perspective, when this many folks are bullish, future returns tend to be a bit on the lower side. But we will also point out that sentiment is much more reliable at market bottoms than trying to call market tops.

Final Thoughts

Markets are certainly eerily calm across many different geographies and asset classes, like a Muskoka lake early in the morning. Maybe it is the calm before the storm or perhaps just the calm before the summer calm. There are certainly positives from an improving trend in the global economy; earnings continue to come in healthy, and inflation is cooling, albeit in a straight line. If the market can continue to ignore the campaign rhetoric leading to the U.S. election, that would be great and unprecedented. At some point, the banter will start impacting markets, but likely not in a positive way. The consumer is getting tired and weighed down by slowing labour gains and inflation, which continues to eat away at previously accumulated savings.

The only thing we are pretty sure of is that volatility will rise in the second half.

Let’s just hope for a calm summer.

— Craig Basinger is the Chief Market Strategist at Purpose Investments

Source: Charts are sourced to Bloomberg L.P. and Purpose Investments Inc.

The contents of this publication were researched, written and produced by Purpose Investments Inc. and are used by Echelon Wealth Partners Inc. for information purposes only.

This report is authored by Craig Basinger, Chief Market Strategist, Purpose Investments Inc.

Disclaimers

Echelon Wealth Partners Inc.

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Echelon Wealth Partners Inc. or its affiliates. Assumptions, opinions and estimates constitute the author's judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. The comments contained herein are general in nature and are not intended to be, nor should be construed to be, legal or tax advice to any particular individual. Accordingly, individuals should consult their own legal or tax advisors for advice with respect to the tax consequences to them.

Purpose Investments Inc.

Purpose Investments Inc. is a registered securities entity. Commissions, trailing commissions, management fees and expenses all may be associated with investment funds. Please read the prospectus before investing. If the securities are purchased or sold on a stock exchange, you may pay more or receive less than the current net asset value. Investment funds are not guaranteed, their values change frequently and past performance may not be repeated.

Forward Looking Statements

Forward-looking statements are based on current expectations, estimates, forecasts and projections based on beliefs and assumptions made by author. These statements involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. Neither Purpose Investments nor Echelon Partners warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. These estimates and expectations involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Unless required by applicable law, it is not undertaken, and specifically disclaimed, that there is any intention or obligation to update or revise the forward-looking statements, whether as a result of new information, future events or otherwise. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional

advice.

The particulars contained herein were obtained from sources which we believe are reliable, but are not guaranteed by us and may be incomplete. This is not an official publication or research report of either Echelon Partners or Purpose Investments, and this is not to be used as a solicitation in any jurisdiction.

This document is not for public distribution, is for informational purposes only, and is not being delivered to you in the context of an offering of any securities, nor is it a recommendation or solicitation to buy, hold or sell any security.

Share this post