Weekly Commodities Report - November 8, 2024

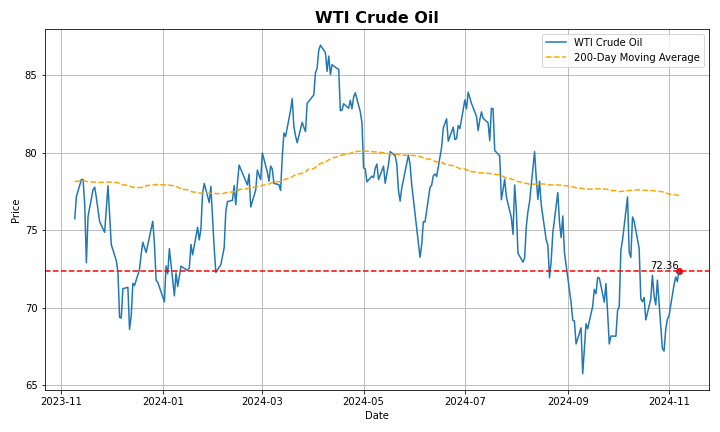

WTI crude oil futures fell below $72 per barrel on Friday but remained on track for a weekly gain as supply risks eased and investors assessed the potential impact of the incoming Trump administration. Hurricane Rafael, which disrupted U.S. crude production, is projected to move gradually westward over the Gulf of Mexico, lessening its impact on oil fields. Downward pressure was further driven by a 9% drop in China’s crude imports in October—the sixth consecutive year-on-year decline—along with rising U.S. crude inventories. Meanwhile, investors believe that a Trump presidency could, on one hand, lower oil prices by boosting U.S. production and imposing tariffs that may weigh on China’s economy, the world’s largest oil importer. On the other hand, Trump’s administration might impose stricter sanctions on oil-producing countries like Iran and Venezuela.

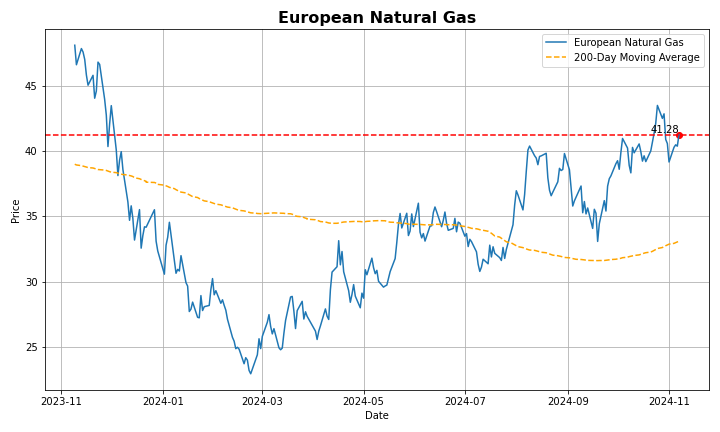

European natural gas futures rose above €42 per megawatt-hour and are on track for a 9% weekly increase due to colder weather forecasts and reduced wind power expected next week. Updated weather models predict temperatures at seasonal averages for the coming days but colder conditions, with some frosty nights, moving in from the east later. This would increase gas demand for power generation due to low wind energy output, prompting more withdrawals from storage, which is currently 94.43% full. Additionally, markets are considering potential impacts from Donald Trump's U.S. presidential win, especially his position on Ukraine and LNG export projects, which could affect future supply. Meanwhile, gas flows from Russia to Europe through Ukraine remain consistent.

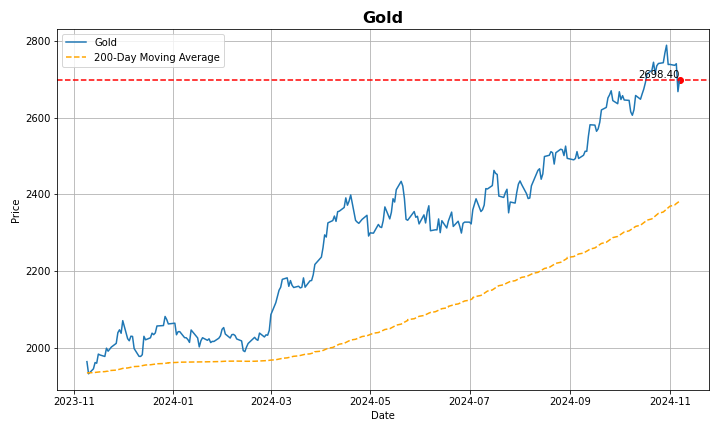

Gold prices eased on Friday but stayed around $2,700 as markets reacted to the implications of Donald Trump’s presidency and the latest Fed interest rate decision. The Fed lowered interest rates by 25 bps as expected on Thursday, while signaling a cautious and deliberate stance on any further rate cuts. Still, markets are factoring in higher interest rates from the Fed, as the new U.S. president's policies—focused on raising tariffs, cutting taxes, and deregulation—are expected to increase deficits and drive inflation. Meanwhile, the demand for gold remained strong. The World Gold Council reported that global physically-backed gold exchange-traded funds experienced inflows for the sixth consecutive month in October. Additionally, gold prices may get an extra boost from new Chinese stimulus aimed at raising local governments' debt ceiling to 35.52 trillion yuan, allowing them to issue six trillion yuan in additional special bonds over three years to swap hidden debt.

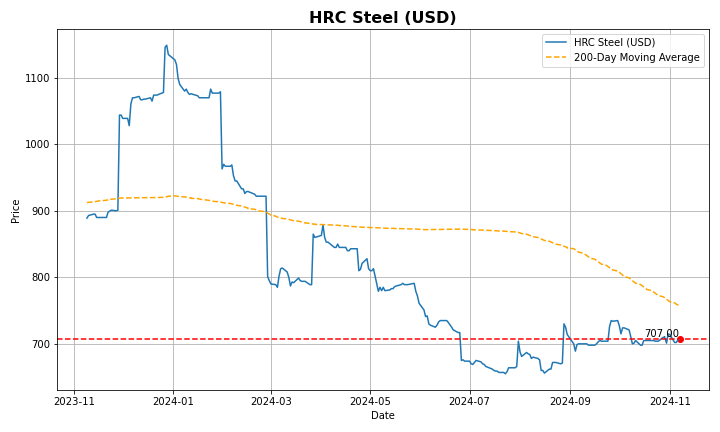

Steel rebar futures slumped to CNY 3,230 per tonne in November, the lowest in over two weeks, as markets assessed the impact that fresh stimulus from China may have on ferrous metal demand. In the conclusion of its week-long meeting, the Standing Committee of the People’s National Congress announced a $1.4 trillion debt package to allow local governments to swap out hidden debt and lower their financing costs to stimulate the economy. Still, the measures underwhelmed investors due to the lack of significant new stimulus, driving steel benchmarks to track the decline in major construction equities. Calls for government support were centered around poor demand for housing in China, which drives major developers to struggle with solvency issues amid poor sales, jeopardizing the health of companies that are among the largest steel consumers in the world. This was underscored by the official construction PMI falling to a record low of 50.4 and house prices sinking by 5.7% annually.

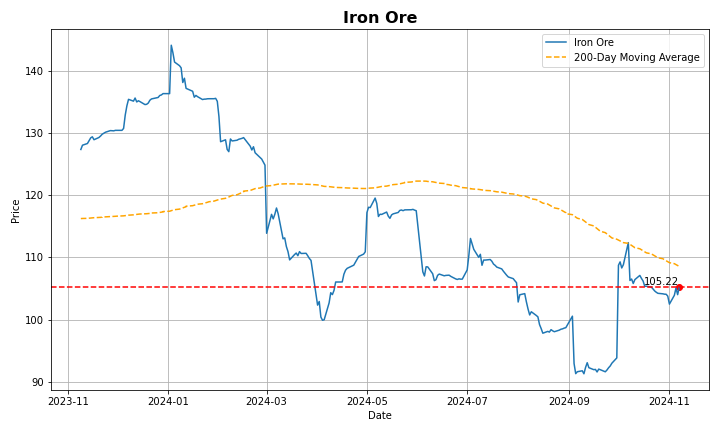

Iron ore prices for cargoes with 62% iron content climbed back above $105 on Friday, driven by investor optimism ahead of expected stimulus announcements from China as the National People’s Congress meeting concludes. The country’s legislature is anticipated to approve significant increases in government debt and spending to stimulate economic growth. Markets are also betting that Beijing will introduce more aggressive policy measures to mitigate the impact of higher tariffs under a Donald Trump presidency. Meanwhile, data released earlier this week showed that China’s trade surplus widened more than expected in October, with exports surging while imports declined, providing further support to the outlook for economic growth.

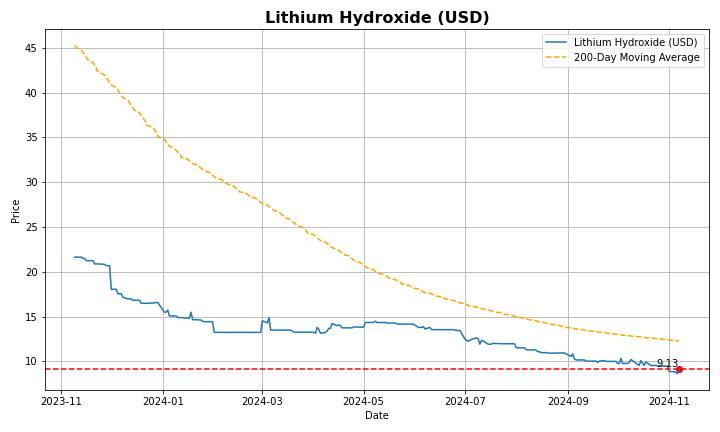

Lithium carbonate prices remained steady since touching the over-three-year low of CNY 71,500 per tonne in late October as overcapacity for electric vehicle batteries in China drove producers to lower asking prices for inputs across the supply chain. Subsidies from the Chinese government triggered a large wave of oversupply of EV batteries and drove carbonate prices to fall 23% this year after an 80% plunge in 2023. Despite the glut, market players expect global supply to soar by nearly 50% this year as hopes of eventual balance drove producers to search for new projects. Chile signaled it would double output over the next decade, and the race to secure battery metals drove China to expand projects in Africa. Also, Rio Tinto aimed to enter the lithium market by buying US-baed Arcadium Lithium for $6.7 billion. Adding to the bearish pressure, the EU placed tariffs against China-based EV manufacturers ranging from 36.3% to 17%.

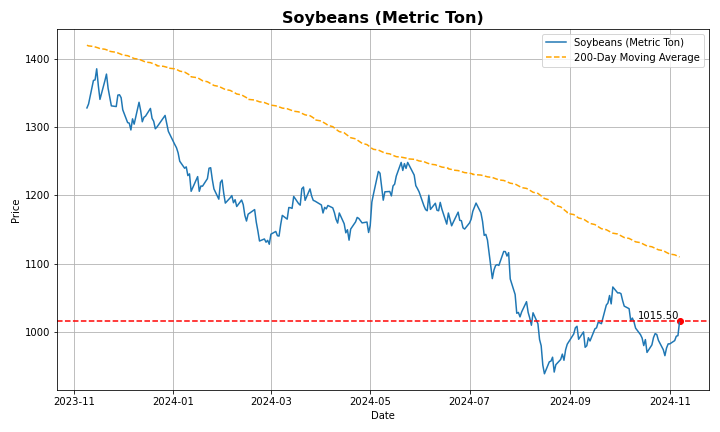

Soybean futures rebounded to $10 per bushel as Donald Trump's victory in the U.S. presidential election raised concerns about potential new trade barriers with China. China, the largest importer of U.S. soybeans, accounts for approximately 40% of total U.S. exports. Despite this increase, prices are expected to decline in the medium term due to ample supply. Argentina’s soybean production forecast for 2024/25 has been raised to 52 million metric tons, with planted area projected to grow by 7% to 44 million acres, marking the largest increase since the 2015–16 season. In Brazil, planting is progressing, with 52.9% of the expected area sown, up from 50.6% at this time last year. Brazilian soybean acreage for the 2024–25 season is projected to rise by 2.8% to 117 million acres, representing the slowest growth in a decade due to lower profit margins.

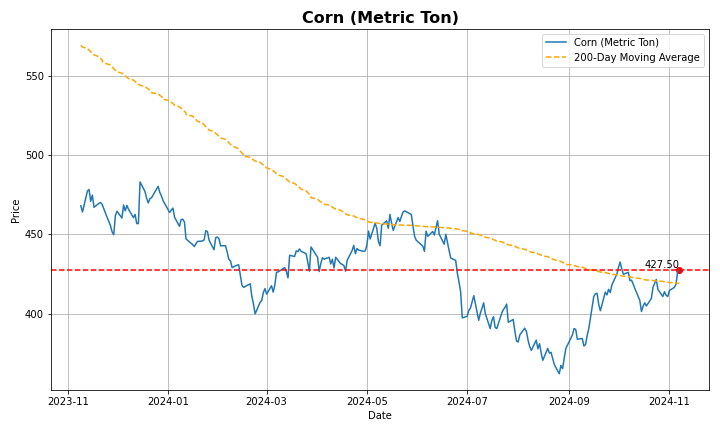

Corn futures rose to $4.20 per bushel, reaching a two-week high amid strong demand and supply concerns. Export demand remained robust, underscored by a USDA sale announcement of 3.9 million bushels for the current marketing year. The weekly EIA Petroleum Status report indicated that ethanol production reached 1.081 million barrels per day for the week ending October 23, an increase of 39,000 bpd from the previous week, while stocks declined by 52,000 barrels to 22.223 million. Current estimates show that corn bushels used for ethanol production are slightly below the USDA's target of 5.45 billion bushels for 2024-25, however, ethanol production typically peaks in the summer when driving demand is highest. Additionally, supply disruptions in Ukraine and the Middle East further impact the market, with concerns over exports from the Black Sea region contributing to global supply constraints and subsequent price increases.

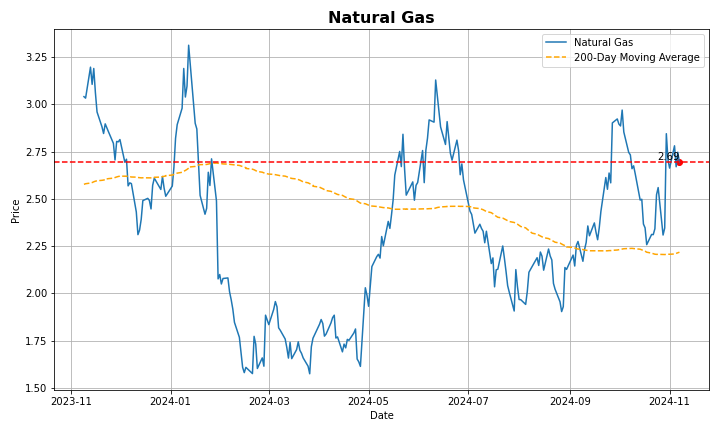

US natural gas futures rose above $2.7/MMBtu, on track for a weekly gain, driven by forecasts for cooler weather and higher heating demand than expected. At the same time, lower production levels due to pipeline issues and Gulf of Mexico curtailments ahead of Hurricane Rafael added upward pressure on prices. The storm was expected to weaken into a tropical storm as it moved across the Gulf, reducing concerns about long-term disruptions. Energy companies had already cut production in the Gulf by about 10%. Meanwhile, the U.S. Energy Information Administration (EIA) reported a 69 billion cubic feet (bcf) increase in gas storage for the week ending Nov. 1, slightly surpassing the forecasted 65 bcf and significantly higher than last year's 19 bcf gain.

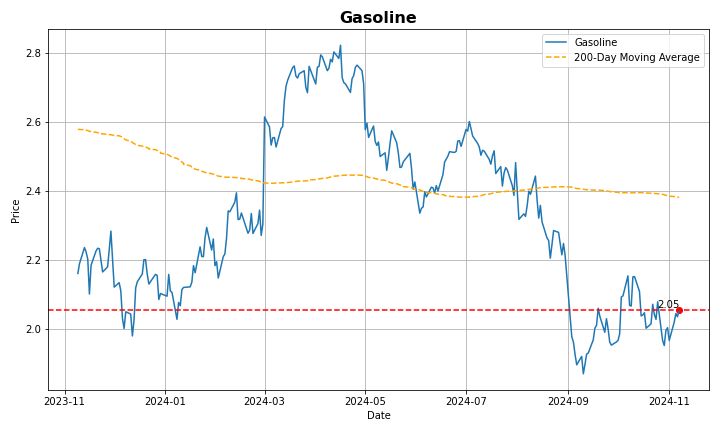

US gasoline futures

fell to $2 per gallon as concerns eased over Hurricane Rafael's impact on oil and gas infrastructure in the U.S. Gulf. The U.S. National Hurricane Center reported that the storm, which had shut down 391,214 barrels per day of crude oil production, is expected to weaken and gradually move away from Gulf oilfields. Additionally, US gasoline demand dropped from 9.15 million to 8.82 million barrels per day for the week ending Nov. 1, while domestic gasoline stocks and production saw slight increases.

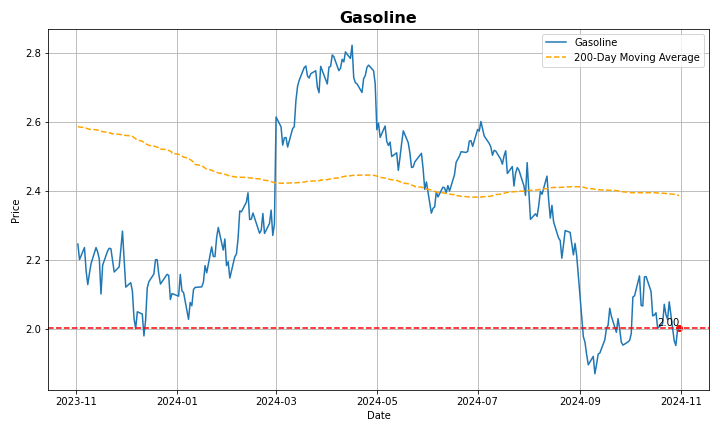

US gasoline futures fell below $2 per gallon, a four-week low, as Israel’s recent strikes on Iran avoided critical infrastructure like crude and nuclear facilities, reducing immediate supply concerns. The restrained nature of the strikes alleviated market fears of major disruptions. As a result, oil prices slumped, with WTI crude oil futures down 6% around 67.5 per barrel. Additionally, US gasoline stockpiles rose by 900,000 barrels for the week ending October 18, defying forecasts of a 1.6 million barrel decline, further pressuring prices.

Silver fell to $31.5 per ounce, approaching the one-month low of $31.2 from November 6th as markets gauged future demand amid underwhelming stimulus from China and the higher rate outlook in the US. The Chinese government announced a package of $1.4 trillion for local governments to swap off-balance sheet debt with Beijing and improve future financing costs, but refrained from announcing new flows of stimulus to specifically target the weak consumption in the economy. This hampered the outlook for industrial metals across all sectors, pressuring silver due to its high usage in electrification, specifically solar panels. Additionally, Chinese-owned solar panel companies reportedly started to cut production after Trump’s election victory in the US threatened higher tariffs in the sector. Trump’s victory also pressured silver by raising the outlook on interest rates as the Fed is expected to keep borrowing costs high to offset expansionary fiscal policy in the upcoming administration.

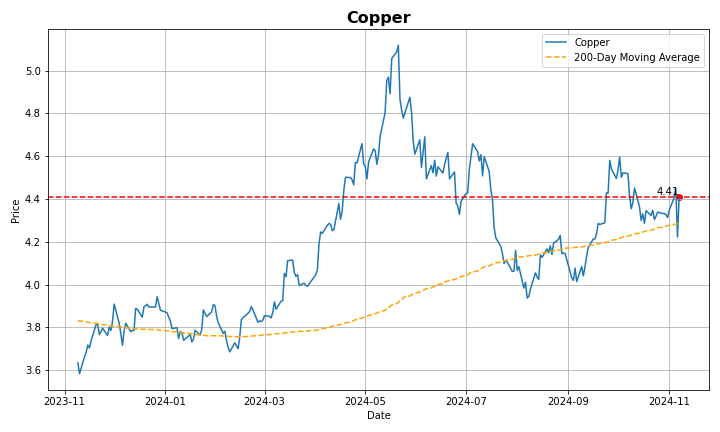

Copper futures sank toward the $4.3 per pound mark on Friday, tracking the sharp decline in base metals as markets were underwhelmed about the outlook on demand after the Chinese government refrained from delivering fresh direct stimulus to its slowing economy. Top policymakers in the National People’s Congress unveiled a CNY 10 trillion debt swap package to assume off-balance sheet debt from local governments and improve their access to cheaper loans. Still, investors showed disappointment over the development of new flows dampened expectations over whether the measure will support manufacturing, hurting the outlook of demand for industrial inputs in copper. In turn, the US dollar held most of its post-election rally amid bets of higher interest rates to rein in expansionary fiscal policy campaigned by President-elect Trump, pressuring commodities priced in the greenback and limiting manufacturing demand from emerging markets.

Aluminum futures

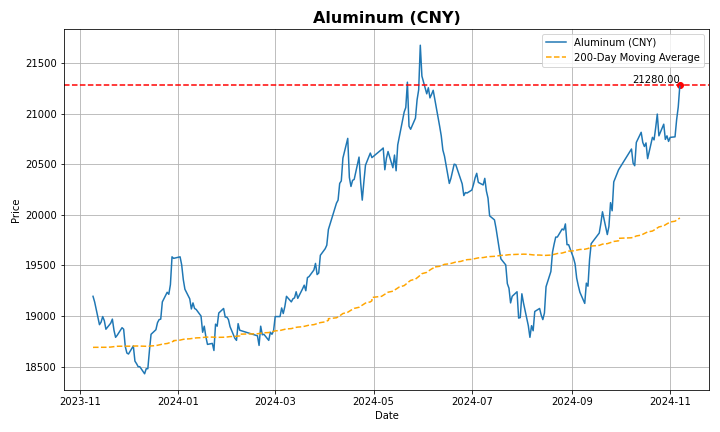

rose to $2,660 per tonne, approaching the three-week high of $2,675 touched on October 25th amid a softer dollar, consistent demand, and increasing supply concerns. The wide range of industrial uses for aluminum prevented the magnitude of sharp declines for the metal due to concerns of slowing factory output in top aluminum consumer China, recently supported by its key role in electric vehicles, solar panels, and other electrification industries. Consequently, aluminum stocks in Chinese ports fell by 20% from their peak in March to 656,000 tons. In the meantime, bauxite prices approached a record high as Guinea blocked Emirates Global Aluminum’s exports from the country. The halt from the world’s top miner added to lower bauxite output from Australia and Jamaica, squeezing Chinese smelters out of their supply and reducing ore inventory to its lowest since 2015.

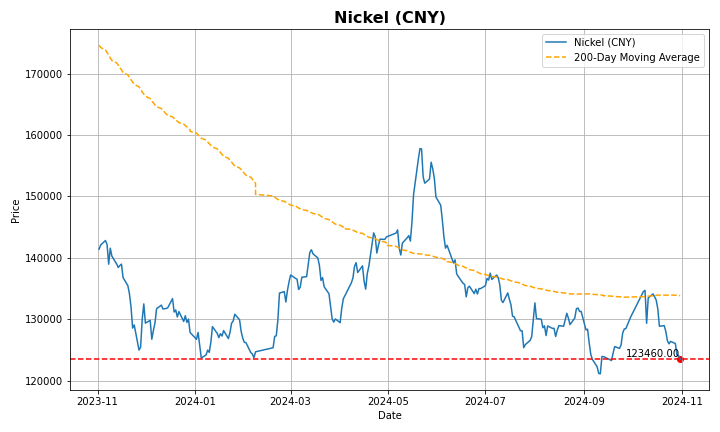

Nickel futures dropped to $15,980 per tonne, reaching a six-week low, with analysts suggesting continued downward pressure due to a significant market surplus and the discovery of nickel at the Wedei prospect in Papua New Guinea. According to the Australian Office of the Chief Economist (AOCE), recent production cuts have failed to lift prices and expects weak demand to keep nickel prices soft through the remainder of 2024. Additionally, rising inventories highlight the oversupply issue, with stockpiles at major exchanges increasing by 90% since the start of the year, driven by production growth in China and Indonesia outpacing demand. Meanwhile, Indonesia, the world’s largest nickel producer aims to manage nickel ore supply and demand to support prices, according to the country's mining minister.

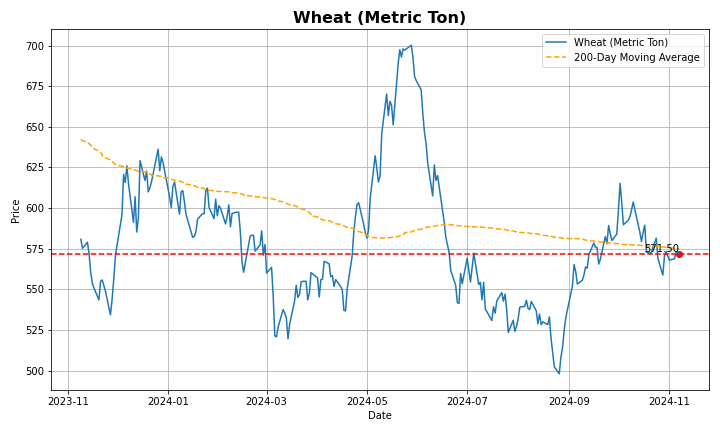

Wheat futures stabilized around $5.7 per bushel following new supply projections, after a brief rise to $5.8 earlier in the week. The USDA projected U.S. all-wheat plantings for 2025/26 at 46 million acres, just below the 46.1 million acres seeded in 2024/25. It also noted that U.S. farmers are expected to increase corn acreage while reducing soybean and wheat plantings for the upcoming marketing year. Meanwhile, Ukraine reported a wheat harvest of 22.3 million tons as of November 8, with Agriculture Minister Vitaliy Koval affirming that winter sowing targets for the 2025 harvest will be met despite difficult weather. Additionally, high Ukrainian wheat exports have added pressure on prices, as grain and oilseed exports by sea and river reached 5.28 million metric tons in October, up from 3.13 million tons a year earlier, according to Ukraine’s UGA traders' union.

Lumber prices rose to $550 per thousand board feet, an over six-month high on supply constrains and as optimistic US economic data lifted the demand outlook for construction materials. US GDP grew 2.8% in Q3, underscoring consumer resilience, while single-family home sales reached a 16-month high and pending home sales saw their largest jump since January 2023. Meanwhile, supply constraints in the southern part of the US drove wood mills to hike prices. Globally, restricted access to affordable wood is worsening the supply shortage in the U.S. Climate-driven infestations in Canada and Europe once helped to bolster the availability of low-cost wood, but now, a combination of reduced logging in Europe, Russia’s export ban, and heightened conservation efforts in North America is tightening the global log supply. This is particularly affecting major markets like China.

Source: tradingeconomics.com, LSEG Workspace, Ventum Financial

© 2018-2023 Refinitiv. All rights reserved. Republication or redistribution of Refinitiv content, including by framing or similar means, is prohibited without the prior written consent of Refinitiv. Refinitiv and the Refinitiv logo are trademarks of Refinitiv and its affiliated companies .Ventum Financial Corp.

www.ventumfinancial.com

Participants of all Canadian Marketplaces. Members: Canadian Investment Regulatory Organization, Canadian Investor Protection Fund and AdvantageBC International Business Centre - Vancouver. Estimates and projections contained herein are our own and are based on assumptions which. we believe to be reasonable. Information presented herein, while obtained from sources we believe to be reliable, is not guaranteed either as to accuracy or completeness, nor in providing it does Ventum Financial Corp. assume any responsibility or liability. This information is given as of the date appearing on this report, and Ventum Financial Corp. assumes no obligation to update the information or advise on further developments relating to securities. Ventum Financial Corp. and its affiliates, as well as their respective partners, directors, shareholders, and employees may have a position in the securities mentioned herein and may make purchases and/or sales from time to time. Ventum Financial Corp. may act, or may have acted in the past, as a financial advisor, fiscal agent or underwriter for certain of the companies mentioned herein and may receive, or may have received, a remuneration for their services from those companies. This report is not to be construed as an offer to sell, or the solicitation of an offer to buy, securities and is intended for distribution only in those jurisdictions where Ventum Financial Corp. is registered as an advisor or a dealer in securities. Any distribution or dissemination of this report in any other jurisdiction is strictly prohibited. For further disclosure information, reader is referred to the disclosure section of our website.

Share this post